There are significant changes to federal student aid beginning with the 2026-2027 academic year due to the One Big Beautiful Bill Act (OBBBA).

Disclaimer: UAB is sharing this information to allow time for students and staff to prepare for the upcoming provisions of the One Big Beautiful Bill Act (OBBBA). The legislative changes under the OBBBA are still pending final outcomes of the negotiated rulemaking process. We will provide additional information as we learn more and if any changes are made. The final rule is expected to be published by June 2026 and will go into effect July 1, 2026.

Changes to Graduate Student Loans

Graduate PLUS Loans

Graduate PLUS loans will be phased out beginning on July 1, 2026. Graduate Plus Loans will not be available for borrowers in new programs or for students who have never used Federal Student Loans.

Exception: Existing Graduate PLUS borrowers can continue to borrow as they complete their current programs. We are referring to this as a grandfathering exception.

- Currently, the new legislation indicates that a student who received any Federal Direct Loan before July 1, 2026 can continue to borrow Graduate PLUS Loans for the same program for up to 3 academic years (or less depending on the expected time to credential).

- Continuous enrollment as indicated by the student’s program is required during each academic year to receive this exception.

New Graduate Unsubsidized Direct Loan Limits (effective July 1, 2026)

Graduate Programs

- Up to $20,500/year, $100,000 lifetime borrowing limit.

- Undergraduate loans no longer count toward this limit.

- Exception: Existing Federal Direct Unsubsidized loan borrowers can access unsubsidized loans under the current limits until completing their current program for up to 3 years (or less depending on the expected time to credential). Borrowers who withdraw or otherwise cease enrollment in their program of study, are no longer eligible to borrow under the pre-July 1, 2026, loan limits.

Professional Programs (Only Medicine, Dentistry, Optometry at UAB)

- Up to $50,000/year, $200,000 lifetime borrowing limit.

- Undergraduate loans no longer count toward this limit.

- Exception: Existing Federal Direct Unsubsidized loan borrowers can access unsubsidized loans under the current limits until completing their current program for up to 3 years (or less depending on the expected time to credential).

Undergraduate Subsidized and Unsubsidized Direct Loans Limits

There are no changes for undergraduate loans, although undergraduate loans will count towards the new lifetime limit of $257,500 combined.

Parent PLUS Loans

On July 1, 2026, Parent PLUS loans for new students will be capped at $20,000 per student per year, with a $65,000 lifetime limit per dependent student.

Exception: Existing Parent PLUS borrowers who have borrowed for their students before July 1, 2026, can continue under the current limits for up to 3 more years or until the student’s program ends or changes whichever is less. Borrowers who withdraw or otherwise cease enrollment in their program of study, are no longer eligible to borrow under the pre-July 1, 2026, loan limits.

Federal Direct Subsidized/Unsubsidized Loans and Graduate Plus Loan Enrollment Adjustments for Less than Full Time Enrollment

OBBBA includes a provision to prorate loan amounts based on enrollment level. This could mean that part-time graduate students (e.g., those enrolled less than full-time) would only be eligible for a portion of the annual loan limit.

- Loan disbursements will be in direct proportion to the number of hours a student is enrolled less than full-time.

- This is effective for the 2026-2027 award year beginning with the Fall 2026 semester at UAB.

- Direct Subsidized, Direct Unsubsidized, and Graduate PLUS loans are reduced for undergraduate, graduate, and professional students.

- Parent Plus loans are not included in this enrollment adjustment.

- Enrollment will be evaluated at the time of disbursement.

- A minimum of half-time enrollment is still required for any Federal Direct Loan disbursement.

Loan Reduction Process

Annual loan amounts will be offered in substantially equal disbursements based on full-time enrollment. Accepted amounts will be divided equally between semesters. However, students will be required to be enrolled full-time to receive the full accepted loan.

Less than full time enrollment will result in a reduced disbursement using a loan reduction calculation.

The loan reduction calculation will be evaluated at the time of disbursement using this formula: number of credit hours enrolled for academic year divided by number of credit hours considered full time for that academic year for the program of study multiplied by 100 equals the reduced annual loan limit percentage.

No reduction is required if a student drops credits after disbursement in current semester but may affect next semester’s disbursement.

Subsequent term disbursements would also be evaluated and reduced based on the total number of credit hours for the academic year.

Note: These rules apply to Federal Direct Student Loans only. Rules for the Federal Pell Grant have not changed.

-

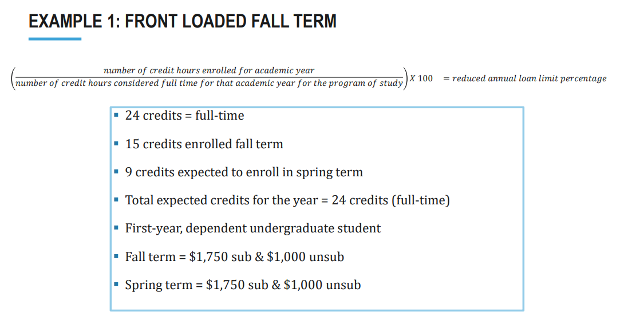

Example 1: Front Loaded Fall Term

Using the loan reduction calculation formula:

- 24 credits = full-time

- 15 credits enrolled fall term

- 9 credits expected to enroll in spring term

- Total expected credits for the year = 24 credits (full-time)

- First year, dependent undergraduate student

- Fall term = $1,750 sub & $1,000 unsub

- Spring term = $1,750 sub & $1,000 unsub

-

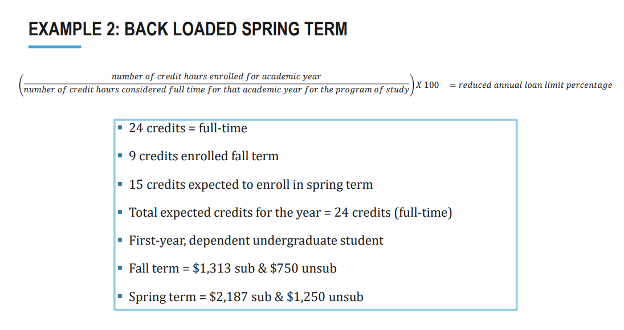

Example 2: Back Loaded Spring Term

Using the loan reduction calculation formula:

- 24 credits = full-time

- 9 credits enrolled fall term

- 15 credits expected to enroll in spring term

- Total expected credits for the year = 24 credits (full-time)

- First year, dependent undergraduate student

- Fall term = $1,313 sub & $750 unsub

- Spring term = $2,187 sub & $1,250 unsub

-

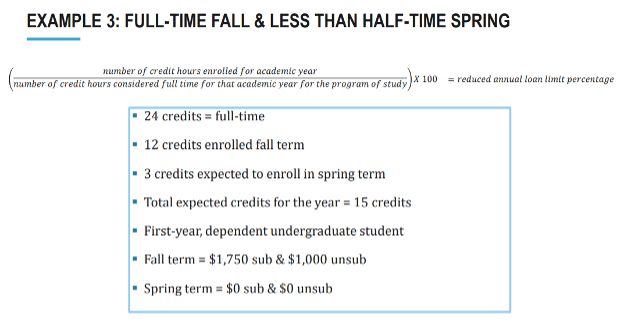

Example 3: Full-time Fall & Less than Half-time Spring

Using the loan reduction calculation formula:

- 24 credits = full-time

- 12 credits enrolled fall term

- 3 credits expected to enroll in spring term

- Total expected credits for the year = 15 credits

- First year, dependent undergraduate student

- Fall term = $1,750 sub & $1,000 unsub

- Spring term = $0 sub & $0 unsub

New Repayment Plans

Federal Direct loans with a first disbursement date on or after July 1, 2026 will be eligible for only two repayment plans: a restructured Standard repayment plan with a repayment period ranging from 10 to 25 years, or a new income-driven Repayment Assistance Plan (RAP) with a 30-year repayment period. This applies to first-time Direct loan borrowers as well as those who have already borrowed Federal Direct Loans for their current programs.

Borrowers with no new loans made on or after July 1, 2026, can continue to be eligible to enroll in the current Standard, current Income Based (IBR), Graduated, and Extended repayment plans, and could also opt in to the new RAP. Current borrowers enrolled in ICR, PAYE, or SAVE plans must transition to a new repayment plan by July 1, 2028. If no selection is made by that date, they will be moved into RAP.

The Financial Aid Office will provide updates to this information as soon as it becomes available.